|

One sector of the procurement services market that has seen much change recently is that of horizontal Group Purchasing Organizations (GPOs). Unlike their vertical GPO and buying cooperative cousins that focus on specific industries, horizontal GPOs offer leveraged contracts for indirect cross-industry spend categories. From being an under the radar sourcing strategy a decade ago horizontal GPOs are making it on to the invite list for more and more indirect spend RFPs. They have also become targets for acquisition. One case in point is OMNIA Partners who through the 2017 acquisitions of Corporate United, Prime Advantage and US Communities created a buying giant that, according to OMNIA's website, boasts a total buy of $10 billion across over 30 industries. Several private equity firms have also been active, either buying GPOs or forming them internally to leverage spend acoss their portfolio companies. When horizontal GPOs first gained traction a decade ago they were primarily targeted at mid-market companies using the "we have discounts you couldn't negotiate on your own" message. What do the recent changes in the horizontal GPO sector mean for those mid-market companies today? To help answer this question I spoke recently with Lisa Wylde, a purchasing manager for Valco US, a mid-market manufacturer of custom fasteners and hardware. In her time at Valco Lisa has utilized regional and vertical cooperatives as well as horizontal GPOs to secure discounts for a broad range of indirect spend categories including facility MRO supplies, industrial gases, uniforms, cleaning chemicals, copiers, office supplies and small parcel shipping. I think you'll agree Lisa's experience throws an interesting perspective not just on how recent events have affected the horizontal GPO's value proposition for the mid-market but also on how that value proposition was perceived originally. Mark Usher: When did you start using pre-negotiated contracts as part of your procurement strategy and what type of providers and contracts were you using at first? Lisa Wylde: When I started at Valco in 2009 we were already using a set of contracts from a regional cooperative of companies in the tri-state area. Valco paid a modest annual subscription to get access to contracts that covered areas like safety supplies, janitorial, personal protective equipment (PPE), small tools, hardware, fasteners, electrical, HVAC and plumbing. The same cooperative also had contracts for office supplies and computers but the pricing wasn't very competitive so we negotiated those on our own. Mark Usher: What type of discounts did you get on the regional cooperative contract and were you able to compare these discounts to the market to see how competitive they were? Lisa Wylde: We were selective in the contracts we used from the cooperative and only used ones we knew had aggressive discounts. Discounts were quoted from a list but the cooperative's contract also listed OEM part numbers. At least once a quarter we'd check price against other regional and the national distributors to make sure the contract discounts stayed competitive. A key point here is that the cooperative agreements were negotiated by someone at one of the regional companies. They had a vested interest in making sure the pricing was good since they were eating their pudding so to speak. Mark Usher: What was your first experience of horizontal GPOs? Lisa Wylde: In 2014 we put an RFP on the street for facility and industrial MRO. We weren't unhappy with our cooperative pricing but at that time but we saw the activity in the MRO vendor market, including horizontal GPOs, and figured we had just enough volume to interest the larger national distributors or GPOs. We left our regional cooperative in the mix and decided to take the approach of wait and see. We were prepared to move all our business to a national player if the pricing and service levels were right but also ready to parcel it out if individual vendors were more competitive for specific sub-categories. We ended up doing the latter by retaining our regional cooperative agreement only for janitorial, safety and electrical supplies (about 30% of the total baseline) with the remaining sub-categories split between a full-line national distributor (about 50%) and a horizontal GPO (about 20%). Mark Usher: What was your criteria for the award and did you calculate a hard cost savings number for the new contracts? Lisa Wylde: We decided to make our delivery requirements and service levels mandatory - essentially pass/fail - then assign 70% weighting to cost and 30% to supplier financial stability. Our feeling was these are non-strategic categories where we are looking for measurable savings and efficiency. Having said that if a supplier can't meet our critical spare lead time then savings are moot. Our split of the business by the various sub-categories was based purely on who provided better pricing. The national distributor certainly won big there but we were quite surprised by the horizontal GPO which was not competitive for many sub-categories and only had lower pricing for fasteners and hardware. Mark Usher: Did you have volume commitments in the contracts? Lisa Wylde: Short answer, no. However in the RFP we provided very detailed historical usage data and stated that future projected usage was expected to be similar within given plus or minus percentages for the different subcategories. We wanted best pricing upfront but did give vendors the option to include quarterly rebates based on trailing quarter volumes. We took these rebates - if offered in the vendor response - into account during the evaluation process by calculating total costs for each vendor under different scenarios of future usage. The regional cooperative and the national distributor provided rebate schedules, the horizontal GPO did not. Mark Usher: So how have things gone since you implemented the new contracts and what are some of your learnings, especially about the horizontal GPO? Lisa Wylde: Overall implementation was smooth. Luckily my commodity manager who led the implementation is very experienced in the roll-out, communications and training areas that can kill you in a contract implementation. So 6 months in we were 80-90% compliant and by a year maverick spend was pretty much zero. We're doing a reasonable job of price compliance although my biggest wish there is that we could change it from an after-the-event audit activity governed by my resources to more of a real-time activity where we know the price is right at the order. The other learning for us is understanding vendor capabilities, particularly for an unfamiliar service model. The regional cooperative - essentially regional vendors - we understand 100%. In fact we both know each other's business as well as the other and very little ever gets lost in translation or negotiation. The full line distributor is straightforward too, he works the volume play. The horizontal GPO I'm definitely still learning though. They can look like a full-line in some categories but then in others they are not competitive. During the RFP process they were very transparent about the fact they extracted fees from their preferred vendors and in some cases where the pricing was close with our regional cooperative I'm sure that fee was what lost them the business for that sub-category. The other reason I am a little wary of the horizontal GPO in terms of a broad match with our needs is that I suspect that their preferred end game may be services rather than product. Their account manager is often positioning value-added services to me like analytics and sourcing support. That's probably in demand from the larger companies but for us we don't have the cost base to warrant what I see as an outsourcing model. Having said that their pricing for our traditional MRO needs worked for 20% of our spend so I want to keep learning their model and their value going forward. Mark Usher: Thank you Lisa for sharing your experience and your insights!

1 Comment

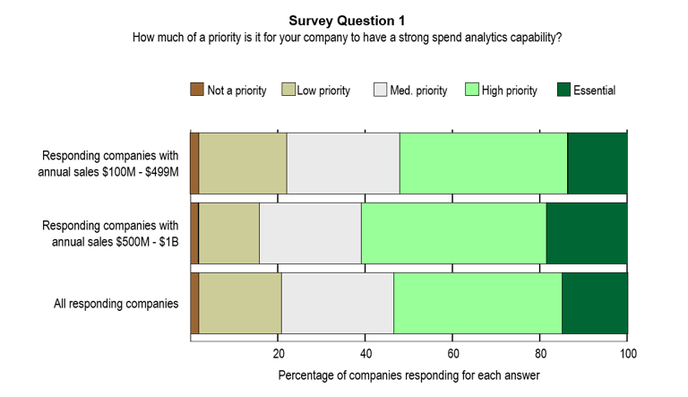

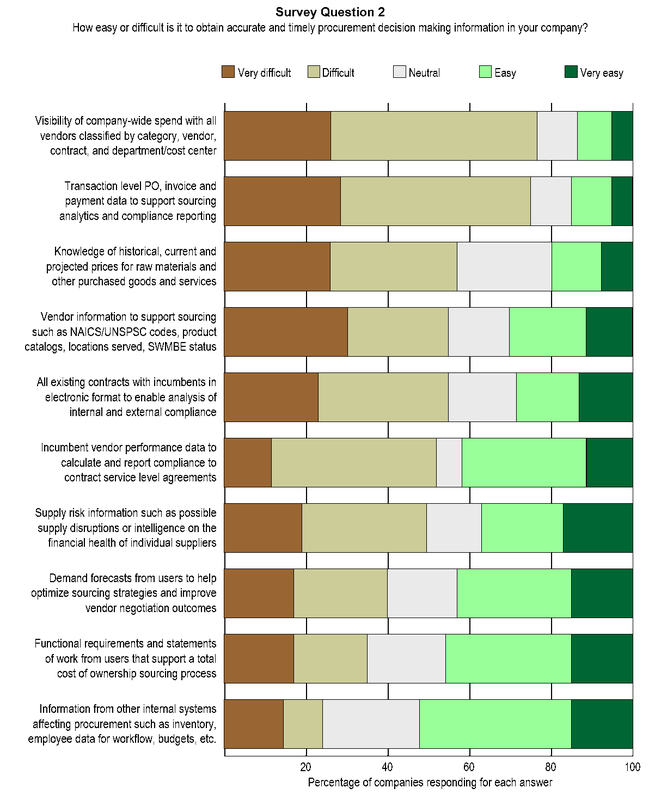

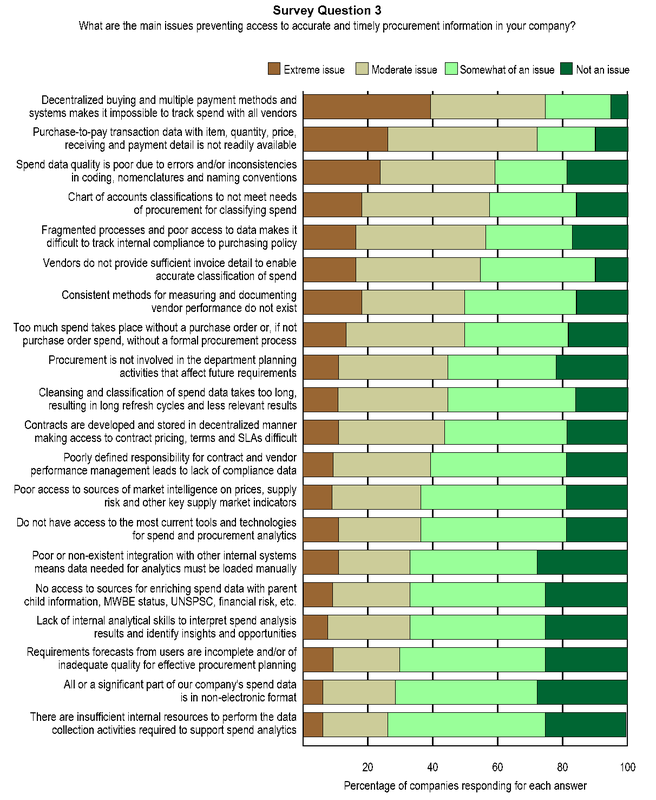

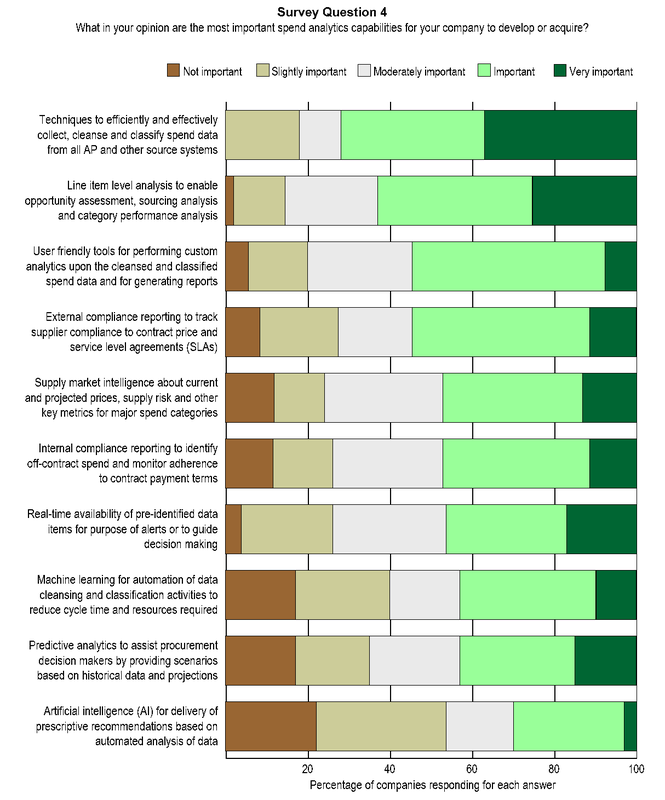

In the first part of my post Is Spend Analytics the Next Consulting Services Money Engine? I discussed my personal opinions and observations about how the current market for spend analytics services seems similar in some ways to strategic sourcing consulting in the 1990s. I also revealed the results of a focus group meeting of 18 small to medium sized companies I hosted in November 2017 that strongly suggested providers might not have a full and accurate understanding of the primary issues and concerns of the mid-market when it comes to spend analytics. In this second part of the post I will present the key findings of a comprehensive survey of the mid-market I conducted earlier this year, the objective of which was to investigate whether the findings of the 2017 focus group were truly representative of the mid-market on a statistically defendable basis. The complete survey report titled Spend Analytics in the Mid Market: The Real Story can be downloaded with a registration on the SpendWorx website but a summary of the survey approach, results and conclusions are provided below. Survey Approach During January and February 2018, I worked with a third party survey company TTL Inc. to issue online surveys to the executives responsible for procurement at 6,717 US companies in all states with annual revenues between $100M and $1B across multiple industry sectors. Usable responses were obtained from the head procurement executives at 419 companies. This equates to a response rate of 6.2%, which is in line with typical response rates for comparable surveys. The three largest industry sectors represented by the respondents were manufacturing (109 companies, or 26%), wholesale (88 companies, or 21%) and retail (71 companies, or 17%). In terms of annual revenues 45% of the companies fall in the range $250M - $499M, 35% in the range $100M - $249M, 13% in the range $250M - $749M and 7% in the range $750M - $1B. Survey Results Survey Question 1: How much of a priority is it for your company to have a strong spend analytics capability? Of the 419 responding procurement executives, some 222 (53%) stated that spend analytics was either a high or essential priority in their companies (see Figure 1 below). Of the 84 executives working for companies with annual revenues of $500M-$1B this percentage increased to 61% (51 companies) confirming the widely held view that larger companies with higher procurement expenditures will generally implement tighter control over their spend. For the 335 companies with annual revenues of $100M-$499M, the percentage of them for which spend analytics was a high or essential priority stayed respectably high at 51%. Figure 1  Survey Question 2 - How easy or difficult is it to obtain accurate and timely procurement decision making information in your company? Here the survey respondents were asked to assess ten types of procurement-related information in terms of the ease or difficulty of obtaining the information in an accurate and timely form in their companies. The results in Figure 2 below show that the three types of information assessed as being most difficult to obtain in accurate and timely form are company-wide cleansed and classified spend, transaction level procure-to-pay data, and market price information. Procurement-related information presenting less of a challenge is internal systems information required to support procurement processes (e.g. financials, inventory, HR. etc.) functional requirements for sourcing, and user demand forecasts. Figure 2  Survey Question 3 - What are the main issues preventing access to accurate and timely procurement information in your company? In this question the survey respondents were provided with a list of 20 commonly faced procurement data issues and asked to indicate the degree to which each was an issue in their own company. It can be seen from the results in Figure 3 below that the issues identified as causing the most problems are strongly correlated with the types of decision making information that are most difficult to obtain in accurate and timely form from Figure 2 above. For example, the top 3 issues in Figure 3 (decentralized buying, lack of detailed transaction data and poor data quality) all directly contribute to the fact that accurate and timely company-wide cleansed and classified spend is the most difficult type of information for procurement decision makers to obtain in Figure 2. Other issues identified as either extreme or moderate by more than 50% of the executives included non-useful chart of account descriptions, lack of detail on vendor invoices, lack of a consistent vendor performance measurement methodology, and too much spend without a purchase order. Issues identified by the responding executives as less of a concern towards the bottom of Figure 3 included insufficient internal resources for data collection, spend data in non-electronic format, poor or incomplete requirements forecasts from users, and lack of internal analytical skills to identify insights and opportunities from spend data. Figure 3  Survey Question 4 - What in your opinion are the most important spend analytics capabilities for your company to develop or acquire? In this final question the responding mid-market procurement executives were provided with a list of spend analytics-related capabilities and asked to identify which in their opinion were the most important capabilities for their company to develop or acquire bearing in mind their company’s unique procurement and data environment. From Figure 4 below it can be seen that over 80% of the procurement executives identified techniques to efficiently and effectively cleanse and classify spend data from all AP and other source systems as either very important or important. Over 50% of respondents further identified line item analysis, user friendly analytics and reporting tools (for working on the already cleansed and classified data) and supplier compliance as capabilities that were also either very important or important for their organizations. Some of the capabilities regarded as lower in importance (at least at this moment in time) included artificial intelligence (AI), predictive analytics and machine learning. Figure 4  Conclusions The survey of mid-market procurement executives produced findings consistent with the November 2017 focus group in a number of areas, namely: Continuing challenges with basic spend analysis issues. The survey confirmed the finding of the focus group related to continuing issues with procurement data. Based on the survey results, mid-market companies still experience significant difficulties in achieving enterprise-wide spend visibility due to challenges in extracting, cleansing and classifying spend data. Advanced spend analytics technologies not yet on radar. A clear finding from the survey was that mid-market procurement executives are more concerned with ‘block and tackle’ issues like cleansing, classification and getting a basic analysis and reporting capability up and running than they are about AI, cognitive procurement or machine learning. The implication is that until the mid-market has spend visibility mastered, the penetration of advanced analytics into the sector will be limited. Smaller companies are on board with the power of procurement. For over 50% of responding companies between $100M-$500M annual revenues to identify spend analytics as an essential or high priority is a clear indicator of how far smaller mid-market enterprises have come in embracing the value of a proactive approach to procurement. Small companies that move first to implement strong spend analytics capabilities stand to gain significant and sustainable cost and profitability advantages over their similarly sized competitors. Lessons for solution providers. Another theme of the November 2017 focus group corroborated by the survey was the perception that technology providers did not understand some of the unique requirements of mid-market companies compared to Fortune 500 companies when it came to spend analytics. The surprisingly low importance placed on the newer technologies in the survey should be a warning to solution providers that the majority of mid-market companies still need help finding their way out of the spend visibility forest. Only then will they be able to look ahead and appreciate the value that the new technologies will bring. The complete survey report Spend Analytics in the Mid Market: The Real Story can be downloaded with a registration on the SpendWorx website here.

Guest Post by Jeffrey Frost, VP Supply Management, Strachan Products Inc. As a contrast to me droning on, I'm excited to welcome Jeff Frost to 1 Procurement Place. Jeff is the VP of Supply Management for Strachan Products, a manufacturer of parts and components for automotive and aerospace OEMs. Strachan Products is also a founder member of Spend Engine, a collaborative procurement community which in full disclosure is owned by my company SpendWorx LLC. It is the subject of procurement communities that Jeff writes about in his fascinating post below. Welcome Jeff! When Mark Usher first approached me last year about the idea of participating in a procurement community I had two immediate thoughts as to what he might be talking about. That it might involve camping out at weekends exchanging purchasing war stories I quickly dismissed. More likely was some type of Group Purchasing Organization (GPO) pooling G&A purchases like office supplies or PCs across member companies. GPOs are certainly something Strachan has looked at in the past but on the times we have evaluated them their pricing has only been marginally better than what we could negotiate on our own. In addition they have always seemed to me to represent one rather tactical component of what could be a far more strategic approach to collaboration. I was very pleased when it turned out that Mark was talking about something a lot closer to this more strategic model with his company's collaborative procurement community. Take the clock forward a few months and I'm only too happy to describe some of the initial benefits and learning that have arisen from our involvement in Spend Engine. First, though I say it myself, our company does most of its buying pretty well. We also don't sweat the small stuff. When we acquired a former federally funded entity in 2009 to bolster our R&D capability we also "acquired" a small team of outstandingly talented procurement professionals who knew indirect sourcing & contracting inside and out. Within six months they had over 80% of our non-payroll G&A expenditure nailed down under aggressively priced blanket contracts with all kinds of contract clauses, market-linked indexes and SLA guarantees to ensure we were always getting the best deal without having to do the three bid-and-a-buy game that steals procurement resources from higher value work. Once indirect was put to bed we turned our focus to where this higher value resided, namely in our direct materials spend. When it comes to our direct spend it's extremely custom and - you would think - as poor a candidate for any type of collaborative procurement as it comes. But that's only if you think of collaborative procurement in traditional GPO-type terms as a group of buying companies pooling volumes to secure leverage-based unit pricing with vendors. That's not what Spend Engine is. Mark Usher can do a far better job of explaining the details of Spend Engine but for Strachan it's allowed us to form relationships with companies that don't necessarily buy the same stuff but that buy stuff with similarly constrained specifications and from supply markets with similar dynamics. Take precious metals for example. We buy significant quantities of platinum to manufacture some of our products. Two other companies in the Spend Engine consortium also buy precious metals, but not platinum. Although we will never leverage spend together in the GPO sense there are numerous common precious metals-sourcing best practices we can mutually support each other in the development of such as management of price volatility, addressing global supply risk, ensuring ethical practices of supply sources, and many others. After just a few months of involvement in the community I can say with certainty that the core business-impacting value captured from this collaboration has exceeded by many times the equivalent value that would be created over the same period from, say, an MRO consortium contract. That's not to say we wouldn't get value from such a contract - one day we might - but the point is that today it is magnification of knowledge that moves the dial for us, not dollar spend. My closing point for procurement organizations thinking of using GPOs or similar approaches is to look beyond the benefits of leverage-based unit price reduction to the higher value that is possible from collaboration with other companies on strategies related to your core business. From experience I can say that for Strachan Products the investment of time in a collaborative procurement community has certainly been worth it and is something that we plan to continue.

When I emerged freshly minted from B-school in the mid-nineties and inserted myself into the flow of warm bodies entering consulting the hot practice area every firm was building was strategic sourcing. Nail your case interview and before you could say "center-led procurement" you'd be pulling down close to six figures driving pivot tables and powerpointing sourcing wave strategies. The attractiveness of sourcing consulting back then was that it represented a way to create a consulting services money engine by billing out highly educated resources to put on steroids a very well defined existing business process - purchasing - that was already being done by existing company employees. Driven into orbit by the "Power of Procurement" large firms and indeed many smaller players enjoyed over a decade of profit taking based on a solid assess-propose-implement methodology backed by a created savings business case model that employed a B-school take on created value even if a little light on dollars in pocket. To give credit where it's due there were a number of laudable accomplishments during this period in areas such as fact-based negotiation and procurement-focused change management. But anyone adopting a truly objective view would have to admit that strategic sourcing consulting in its heyday was optimized around a repeatable one-time service delivery model rather than the creation of a sustainable capability for the customer. The main reason sourcing consulting growth eventually plateaued was that many of the former consultants who led the charge in the nineties became VPs of Procurement who now saw the service they used to deliver as a laser-focused gap filler rather than a turnkey solution. Sourcing consulting is by no means dead but is more pragmatically applied. More useful in fact.  Is spend analytics the 21st century version of the 90s era strategic sourcing money engine for consulting firms? Working with clients over the last 2-3 years I began to notice echoes of the nineties sourcing consulting phenomenon in spend analysis, or shall we say spend analytics as it more commonly referred to today. Rarely can a week go by without a blog post or white paper addressing the transformation and extension of spend analytics beyond just the building of spend cubes to end-to-end procurement and supply market intelligence. Enterprises, we are told, must engage the power of AI to fully leverage the explosively increased quantity of decision making information available to them. The smallest surprise of all is that a legion of providers are at the ready to deliver the services that are surely needed to tap this newly available procurement power source. The question companies should ask however is whether these services represent a timely response to customer needs or whether they are primarily a provider model designed to opportunistically tap a market. They could and probably should be both of course, but it’s the relative weight of each that’s important. In November 2017 I met with a focus group of 18 Southern California procurement executives to capture input for a presentation I was preparing on the subject of spend analytics in the mid-market. The companies represented ranged in annual revenue from $250M to $900M and operated in industries that included healthcare, industrial manufacturing, financial services, retail and telecommunications. In addition to the numerous learnings and insights shared by individual executives based on their company experiences, three findings surfaced during the day that were notable by the fact that they were relevant to the majority of the companies present:

On the face of it these findings seemed to support my earlier anecdotal observations of the newer provider solutions not being in tune with customer requirements, at least in the mid-market. Following the meeting I decided to investigate whether the focus group findings were representative of the mid-market as a whole and whether, in general, conclusions could be drawn that were defendable statistically. To this end I worked with a third-party survey company TTL Inc. during January and February 2018 to issue an online survey to the executive responsible for procurement at 6,717 US companies with annual revenues between $100M and $1B across multiple industry sectors.

In part 2 of this post I will present and talk about the findings of this survey and the implications of these findings for companies and providers alike. (Note: the names, client details and even spend categories in this post have been changed to protect the “not so innocent”!)

Following on the heels of my posting “Can a Spend Analysis Have an ROI?” I feel obligated to provide a living breathing example of a situation where someone – in this case a consulting firm - decided NOT to do a spend analysis but plow ahead with sourcing. Okay, it wasn’t just any consulting firm – it was the firm that yours truly was working for at the time (but I’ve worked for so many you’ll never guess which one). And okay, it wasn’t just any project at this consulting firm but it was the project that I was working on at the time. Shame on you, Mark. But hey - I was young and I definitely needed the money! Anyway here’s the back-story. Our firm had just won a major strategic sourcing project for a $5B consumer products company. Big – about $1.5M in total fees for sourcing of seven spend categories including office supplies, MRO, temps, janitorial services, PCs, corrugated packaging, and travel. How do you think we picked the Magnificent Seven? They sound the typical band of villains, right? Well, it was a very scientific process that unfolded late one Thursday afternoon in the middle of a mid-west summer. I know it was a Thursday afternoon because we would fly in to the client on Monday mornings and fly home Thursday night, and I remember the meeting where the Seven were picked took place just before we all grabbed our taxis for the airport. My Partner and I were sitting with the client’s VP Procurement and a snippet of the conversation went something like this: CONSULTING FIRM PARTNER: Well Chris, looking at the GL numbers from Charlie (Charlie was a Financial Analyst in Accounting) I’d say we have seven candidates that look perfect for strategic sourcing. CLIENT VP OF PROCUREMENT: What’s the rationale, Brian? CONSULTING FIRM PARTNER: Well we usually find that the best categories to pursue are the ones with reasonable spend that haven’t been sourced – that means higher savings – and ones that also don’t present too much of a challenge from a complexity or stakeholder resistance point of view. That way you stand the best chance of capturing some decent benefits while also building the skills and confidence in your organization for taking on more challenging categories later. CLIENT VP OF PROCUREMENT: Makes sense. So these are the categories? (Looks at the list of the Magnificent Seven). Total spend about $100 million…….that would net us about $10-15 million savings from your estimates, right? I like it. What’s next? Your team will create the detailed work plan? CONSULTING FIRM PARTNER: Mark’s on it. What happened next? Well it turned out that three of the categories proved to be massive disappointments after we found that the spend available for sourcing in each of these categories was much less than what had originally been thought. Embarrassingly less, in fact. The reason for this was very simple – the accounting data used to make the sourcing decisions (spend by general ledger code with a few cuts of spend by supplier) had failed to provide the necessary detail and accuracy to make an informed decision. What should have happened? We should have conducted a spend analysis to cleanse the accounting data and classify it into commodity groups based on all the clues available such as vendor name, GL code and cost center. Where we didn’t have enough clues in the data to break out a commodity we should have asked the using departments to help clarify what had been spent with whom. Oh, and we should also have asked whether there were any planned reductions in usage in any of the categories. If we’d done that we would never have picked three of the Magnificent Seven, would never have wasted months of our time and the client’s time chasing minuscule benefits (one category was canned early on, but the other two were continued largely to save face) and – most important – would not have disappointed our client. What really happened in this case? We believed Charlie from Accounting! Now Charlie is a good guy and does good work. His accounting data works fine for financial reporting and budget planning. But in its raw form it just doesn’t cut it for making effective major resource deployment decisions during the planning of a strategic sourcing program. To accomplish this you need to invest in a spend analysis to transform Charlie’s numbers into meaningful purchasing intelligence. Ignore this advice while recruiting your next “Magnificent Seven” and you may find yourself riding into Sourcingville firing blanks with Charlie watching safely from the saloon. Originally published in response to Michael Lamoureux's Seven Grand Challenges of Supply and Spend Management in 2008. 1. Continue the Strategic Elevation of Procurement

Although much progress has been made in this area there is a lot more to do, particularly in the mid-market and in the public sector. The motherhood and apple pie statement here is “procurement strategy must be an integral component of corporate strategy” or something similar. This is the truism but the hard fact of life is that procurement must do the work internally to make itself worthy of such a lofty positioning. Technical and leadership skill levels must dramatically improve in many procurement departments, salaries must be raised to attract talent, and ultimately the procurement function must be respected and held in awe by internal stakeholders and suppliers alike as a focal point of bleeding edge sourcing practices. 2. Achieve a Truly Seamless Cross-Functional Strategic Sourcing Process What I DO NOT mean here is inventing another seven-step consulting methodology. What I do mean is reaching a state where the right organizational players are facilitated smoothly into the strategic sourcing process at the exact time that their respective value-adds are required. This could be Engineering during specification rationalization, Manufacturing during supplier capability assessments, or Legal during contract development just to give a few examples. Procurement with its overall end to end responsibility for the sourcing process is in the perfect position to perform this facilitation activity, provided of course it possesses the skills and organizational credibility to perform this task effectively. 3. Optimize the Outsourcing of Indirect Materials Enterprises will continue to evaluate their investments in the indirect procurement area. Some of the decisions they will ponder include which spend categories to outsource, which processes to outsource for these categories (sourcing? spot buying? purchase order processing? category management?) and whether to utilize “semi-outsourcing” strategies such as Group Purchasing Organizations. My personal belief is that very few organizations will outsource procurement “lock, stock and barrel” but that many will outsource selective processes for selective categories on an as-needed basis, sometimes utilizing more of a staff augmentation model than true outsourcing (“hiring commodity mercenaries” as one of my customers termed it). I also predict more use of accelerated, quasi- outsourcing techniques such as pre-negotiated contracts, particularly in the mid-market and private equity sectors. 4. Pursue Enterprise-Wide Spend Visibility Organizations will continue to struggle in their quest to obtain visibility of who buys what from whom at what price across the enterprise. Without this knowledge they will be unable to effectively leverage their total spend with suppliers. Some enterprises will continue to believe mistakenly that they will be able to drive all spend through a single e-procurement system and achieve global visibility that way. The leaders in this area will realize that they need a tool to consolidate and analyze data from all systems that could potentially contain valuable spend information whether they be e-procurement systems, accounts payable, p-card or other sources. Oh, and the smart organizations will also realize that you don’t pre-select spend data for analysis based on accounting codes (see A Cautionary Tale of Zero Investment )! 5. Pragmatically Manage All Elements of Supply Risk Talk about buzz. This one has rattle & hum. Personally, I see a little too much talk of virtual reality dashboards and not enough about what is really important. This means identifying the 20% of uncertainties in the supply chain that drive 80% of service and cost performance and figuring out how to provide accurate and timely information on these uncertainties to commodity managers to guide them in their supply management decisions. I would be ecstatic if organizations would simply improve internal reporting of incumbent performance, routinely subscribe to third party supply risk data sources, and implement formal methodologies for assessing the total cost impact of alternative global sourcing strategies that holistically consider all financial, quality and physical supply chain variables. I agree that the sky is the limit in this area, but let’s get the basics nailed down first. 6. Maximize the ROI of Sourcing and Procurement Technology Oh so much to relate, so little space. The ongoing headaches here will include answering such questions as “Why do I need an e-sourcing tool if I always get good results with a traditional RFP?” or “Do I really need a spend analysis tool if I have an analyst who’s a wizard with pivot tables?” or “should I buy e-procurement or use my ERP purchasing module?” Those organizations that realize the greatest ROI from their procurement technology investments will be those that ground their decision-making in good old Procurement 101 fundamentals. If your solicitation meets the criteria for a low risk, competitive bid commodity like office supplies then try out a price-focused reverse auction. If you are preparing for a complex RFP such as LTL freight then ask an e-sourcing provider to demo an e-sourcing optimization event. Take stock of where the tool adds value over your standard approach and where it doesn’t. If it doesn’t, stay with what works (though you may be surprised). As for e-procurement, stay grounded in what will ultimately drive most spend through your preferred supplier contracts. Compliance is all about users finding what they want quickly and easily, not about the color of the swoosh or the sound of the bells and whistles. If you are in a state of paralysis by analysis, consider a hybrid approach that utilizes the best of the ERP and the e-procurement worlds (see The Age of e-PERP ). 7. Make Procurement “Sick” The supply management profession must make itself attractive to young, degreed job seekers who would typically shun a career in Procurement for something more Generation X/Y such as, well, almost anything really. This challenge will revolve around positioning Procurement as a business function that someone can use as a launching pad to progress to the highest echelons of an organization, even the top job itself. This is still a far cry from how “Purchasing” is viewed today, with the exception of a few leading “Medal of Excellence” companies such as United Technologies, Proctor & Gamble and Hewlett Packard. I won’t be satisfied with our progression in this area until the day my college-bound daughter comes home excitedly babbling to me about how she is so, like, awesomely looking forward to embarking upon her Ivy League college experience in the field of Strategic Supply Management. The most generally accepted value proposition for e-RFx solutions (whether reverse auction, optimization, or online RFP) is their ability to rapidly and effectively drive lowest total cost sourcing decisions through whizz-bangs such as “competition-inducing online bidding environments”, “optimization tools facilitating real-time multi-attribute evaluation”, or one of my personal favorites “a geography-negating virtual collaboration medium where buyers and suppliers can participatively create value-maximizing supply solutions”. Phew, I’d buy it.

The above is all true of course; e-RFx solutions really do help procurement organizations identify and implement lower TCO sourcing strategies than they could before and in less time. One of the oft-overlooked additional advantages of e-RFx technology however is that it also supports the implementation and consistent use of a single, consistent, best practice strategic sourcing process. As an example I have been working recently with a company that decided to transform its procurement department from a tactically focused buying function to a best-in-class strategic sourcing organization. One of the problems that this customer faced was that the quality of the contracts developed by its procurement department varied tremendously depending upon who was doing the contracting. This was because each buyer followed a different sourcing process. One buyer would gather detailed usage and requirements information, develop a structured RFP document, and then follow a formal process to issue the RFP, evaluate responses and make the contract award. Another buyer, for the same or a similar commodity, would follow a far more informal process involving only very rudimentary requirements gathering, issuance of a short bid document to suppliers via email, and a rapid award of business to the successful vendor. The point is not that either sourcing approach is necessarily wrong but that there had been no attempt at this company to define and implement a single process that was agreed to be the best practice sourcing method for that commodity. The beauty of today’s leading e-RFx tools is that they provide functionality that effectively guides (one could even whisper softly “force”) the buyer through each step of a sourcing process that has been pre-defined as being “best practice” for that commodity. So for a price focused commodity like office supplies a leading e-RFx tool will “guide” the buyer through a sequence of steps including completion of a requirements template that provides suppliers with key data such as projected usage and delivery locations, execution of a reverse auction to set core list prices and off-core discounts, collection of key supplier information, and post-auction evaluation of price and non-price factors. For a more complex commodity such as print, the set of steps could include optimizing the award of business by print sub-category to take into account the fact that one printer can be more cost effective in certain types of print processes than another. For an organization that currently has fragmented and inconsistent approaches to sourcing, e-RFx tools provide an excellent way to define and formalize standard processes for these and other types of commodities. Of course, e-RFx technology alone will not drive the creation of best-in-class contract and supplier relationships. In many cases there will also need to be a step change increase in buyer skills sets to enable effective management of the underlying sourcing process. That being said, I would recommend that any organization currently seeking to implement strategic sourcing best practices consider the role that today’s e-RFX tools (and also e-RFx’s “sister” e-tools of spend analysis, e-procurement and contract management) can play in helping to support the roll-out and consistent use of a standardized, high quality procurement process. Don’t get me wrong, TCO is clearly king when it comes to the business case for these tools. But the comfort of knowing that everyone in the company responsible for making major supply decisions is using the same high quality process is surely a BIG bonus. Remember...as dear ole Ted Turner would say, or sort of....."Early to bed, early to rise, work like hell and standardize!" Many of you will have learnt from the auto bailout news coverage that GM, Chrysler and Ford between them owe about $10B to their suppliers. You may also have learnt if you did not know already facts such as the following:

-Parts and components provided by auto suppliers (car seats, dashboard consoles, doors, windows, axles, wheels, brakes, etc.) constitute over 70% of the cost of a vehicle rolling off the production line in Detroit. -While GM, Ford and Chrysler employ 239,000 people in the United States, the country’s 3,000 or so auto suppliers employ more than 600,000 workers The "so what" about the above two nuggets is that the "auto industry" DOES NOT EQUAL GM + Chrysler + Ford although you would never have thought so from either the news coverage or the way that the recent $17.4B emergency bailout package was doled out. The Big 3 comprise CONSIDERABLY LESS THAN ONE HALF of the auto industry by either of the two measures above. And yet there is absolutely no guarantee that those auto suppliers in the greatest financial distress and/or those that are most critical to the auto industry supply chain will receive one penny of the initial $13.4B to be distributed to GM and Chrysler. Them two's got their own executive salaries and UAW wages to pay first. Auto suppliers will be paid strictly on a "what's left over" basis. By way of an additional industry insight, I was speaking to a friend of mine who works at one of the auto industry's major tier one suppliers (i.e. one that sells auto assemblies and components directly to one of the Big 3) who told me that of the $10B owed to the auto suppliers over 50% consists of payables that are aged over 90 days. He also told me that many of the industry's lower tier suppliers (those that sell to the tier ones) are facing payment terms of net 120 days or worse (payment term lengths magnify as you go further down the supply chain). In other words they just don't get paid. It's not surprising then that hundreds of these lower tier suppliers have either gone out of business or will be out of business in the early part of 2009. To make matters worse many of these suppliers produce critical parts and/or tooling that could bring the entire auto supply chain to a halt if they are delivered late (or worse, not delivered at all) to a tier one vendor. Okay so I'm being long winded again, what is my point here? My point is that surely there should be some type of strategy in place to guide the bailout funds to those parts of the auto industry supply chain that are most critical to driving higher levels of financial and operating performance for the industry as a whole. Sure, a substantial part of this should go to GM and Chrysler. But from my argument above, less than half. When President Elect Obama takes office he should form a Bailout Funds Distribution Team of auto industry experts to define a financial rescue package that ensures money is distributed among the Big 3, key tier one suppliers and supply chain-critical lower tier suppliers in a way that positively impacts holistic demand/supply chain performance metrics. Leave the distribution of bailout money up to the executive suites of GM and Chrysler and with what's left for auto suppliers you'd be lucky to be able to afford a year's subscription to the Jelly of the Month club. Welcome to my next surefire strategy for bewildering your customer with your ability to snatch defeat from the jaws of consulting project victory. Strategy #9 is an oft-followed approach that goes something like this

1. Prime contractor wins a major piece of business following an RFP process 2. Prime contractor now realizes that he won't be able to do all (or in some cases ANY) of the work that he so creatively described himself as being able to do in his RFP response. This could be for a number of reasons including but not limited to: - he doesn't have the expertise required - he doesn't have the bandwidth or the staff to do the work himself - he would rather spend time selling the next piece of work rather than deliver this one 3. Prime contractor rapidly finds and hires a subcontractor (who is generally an expert in the work that has been sold) to do the work. Prime contractor reviews proposal with subcontractor, provides cursory explanation of promised deliverables, and negotiates hourly rate for subcontractor to complete the work while still leaving a fairly attractive profit margin for himself. 4. Prime contractor leaves subcontractor to do the work while he, well, does something else. ............................TWELVE WEEKS LATER............................ 5. Prime contractor returns from Maui and drives directly from LAX to client site to meet with subcontractor for review of final deliverables. On arrival at client, prime contractor is horrified to learn that: - Project is four weeks behind schedule - Subcontractor has already billed an amount equal to your budget and is demanding additional payment to complete the project - Subcontractor's travel expenses are equal to 40% of project fees - Customer is withholding your final payment pending delivery and acceptance of the final deliverable, still four weeks away 6. Prime contractor fires subcontractor and completes the work himself. In some cases the prime contractor will even need to hire another sub if the work requires expertise completely outside of his comfort zone, making the project economics even worse. Results? Late and sub-par deliverables, miserable profit margin, and - perhaps worst of all - a very unimpressed client who will likely hire their mother-in-law rather than you the next time they need a consultant. What went wrong? Well, by following "Surefire Strategy #9 for Producing a Consulting Train Wreck" the prime contractor above completely failed to adhere to some of the cardinal rules of SUBCONTRACTOR MANAGEMENT, namely: Rule 1: Clearly identify subcontractor requirements for your project DURING THE SALES PROCESS and identify and shortlist subcontractor candidates well in advance of you winning the work and certainly well before kicking the project off. Rule 2: Should you win the work, interview your shortlisted subcontractor candidates. Evaluate them based on their understanding of the project's deliverables (which you will VERY clearly define for them) and their ability to persuade you of their expertise and capability to deliver. Rule 3: Negotiate compensation with your selected subcontractor whereby payment is tied to the SUBCONTRACTOR COMPLETING DELIVERABLES THAT ARE ACCEPTED BY THE CUSTOMER. That way, even if you are indeed in Maui, the sub has an incentive to produce high quality and timely deliverables. Rule 4: For goodness sake, demand at least twice-weekly status reports from your subcontractor during the project. Preferably, visit the project site at least every other week. Rule 5: STAY IN TOUCH WITH THE CUSTOMER. Although you are outsourcing the delivery of the work, NEVER OUTSOURCE THE CUSTOMER RELATIONSHIP. Put in at least a weekly call to your main client sponsor to make sure that she is happy with the progress of the project. Remember, the customer doesn't necessarily need to know that your subcontractor is actually a subcontractor (unless, of course, you are bound by the terms of your contract with the customer to disclose this) - for all they know the subcontractor is one of your employees. And you would always keep on top of the work of one of your employees, wouldn't you? In other words, AVOID AT ALL COSTS Surefire Strategy #9 for Producing a Consulting Project Train Wreck – “Sub Out Major Parts of the Work, Go Do Something Else, and then Check in With the Contractor at the End”!! Implement the antithesis of Strategy #9 instead! In this particular case, this means following the CARDINAL RULES OF SUBCONTRACTOR MANAGEMENT above. Are you getting into the swing of this "Implement the Antithesis" thing yet? Good!! Next week, visit 1Procurement Place for Surefire Strategy #8 for Producing a Consulting Train Wreck - "Just Focus on Things You Can Control - You Can't Be Blamed for the Actions of Others". Would a private equity firm ever think about investing in a company without conducting a comprehensive analysis of its ability to generate an attractive future return? Of course not! A friend of mine in private equity once told me that for every one hundred million dollars a PE firm invests it has spent a million dollars in internal salaries and due diligence consulting fees analyzing the deal prior to pulling the trigger.

In a somewhat similar vein, would you ever think about buying a new or used car without carrying out at least a rudimentary analysis of the comparative reliability and performance of the various models? I didn’t think so. If you’re like me, in addition to burying yourself in Consumer Reports you also spend all the weekends between February and July test driving every vehicle under the sun until your significant other finally explodes “enough already – make up your mind!” What about hiring someone for your company? You wouldn’t make an offer to a person without a rigorous evaluation of their capability to perform the job would you? You pick apart resumes, fly candidates in for interviews, give them case studies, call their references, and conduct drug screens and background checks before extending an offer. What’s the common theme in each of the above examples? It’s that in each case someone is making an investment of money (the due diligence consulting fees, the job candidate travel expenses) or time (lost family time at weekends doing test drives, lost work time interviewing candidates) to gather information critical to a particular decision making process. The return on the investment is an increased probability of a favorable outcome from the decision – a higher profit when the PE firm sells the company three years later, a pleasurable ownership experience for the car buyer, and a high performing employee for the hiring company. So Mark, I hear you all saying exasperatingly, what the Sam Hill does all this have to do with spend analysis? Quite simply, numerous companies of all sizes across many industries are making high dollar resource deployment decisions in procurement while having little or no access to a piece of information that is critical to the procurement decision making process. That piece of information would be about SPEND. Information providing answers to massively important questions such as: What is total spend? What is spend by commodity, supplier, and department? How much spend is currently under contract, in total and within each commodity? How many suppliers account for the top 80% of spend in each commodity? With how many different departments are your highest spend suppliers doing business? How much spend in each commodity is with non-approved suppliers? Which departments are responsible for the non-approved spend? Only by having answers to these type of questions will an organization be able to identify those commodities, suppliers and departments where the application of scarce procurement resources will yield the highest return. How does an organization get these answers? By conducting a SPEND ANALYSIS, a process for producing a consolidated and accurate view of an organization’s purchasing expenditures by commodity, supplier and department. I won’t go into the intricate details of the spend analysis process here or the various tools available in the market to conduct one but, yes, to perform a spend analysis you will need to….make an investment! Depending on the approach you take the investment will take the form of people cost to conduct an internal analysis, software license fees for a tool, consultant fees, or a combination of all of these. The key is to perform an effective spend analysis that allows your procurement organization to focus its people, processes and technologies in the areas that will yield the greatest benefits. Examples of such areas are commodities with the highest total spend across the enterprise, commodities with too many suppliers, suppliers doing high volumes of business with different departments, and departments spending large amounts with non-approved vendors. One of my clients with $500M of total spend recently conducted a spend analysis that identified just over $100M of spend with opportunities for sourcing, incumbent renegotiation and maverick spend reduction. Following the spend analysis this company focused its best and brightest commodity managers exclusively on this $100M and realized $28M of annualized cost savings. Without the spend analysis the same talent would have been wandering blind amongst the $500M and would have been very lucky to have found half of the $28M. Let’s say they were very lucky and found over half, say $18M. That would still mean that conducting the spend analysis had led to an additional $10M of savings. And what did the spend analysis cost? Less than $100K in software and services. Guess what, there’s a spend analysis ROI. And an attractive one at that. You would be surprised (unless you get to see as many procurement departments as I do) just how many companies today are not able to identify the opportunity areas described above, and by inference are not able to prioritize the deployment of their procurement resources. Many of these companies will tell you they know where the cost savings are. They’ll tell you they know their business and that they know where to look. But they don’t really. They guess where to focus their people. They roll the dice on where to conduct a reverse auction. And they come up with dry holes again and again. Why? Because they haven’t invested. They haven’t done the due diligence. They haven’t test driven the commodities. They haven’t fully evaluated the candidates. They haven’t done a spend analysis. |

1 Procurement Place

Non-spin commentary on the world of procurement, supported every now and then by the occasional piece of factual information. Mark Usher

Mark is Founder and CEO of SpendWorx LLC, a provider of spend analytics services. Prior to SpendWorx Mark co-founded Treya Partners, a boutique procurement consultancy. Earlier in his career Mark held various positions at Accenture, GE Aviation and Rolls-Royce.

Archives

December 2022

|

RSS Feed

RSS Feed